Executive Summary

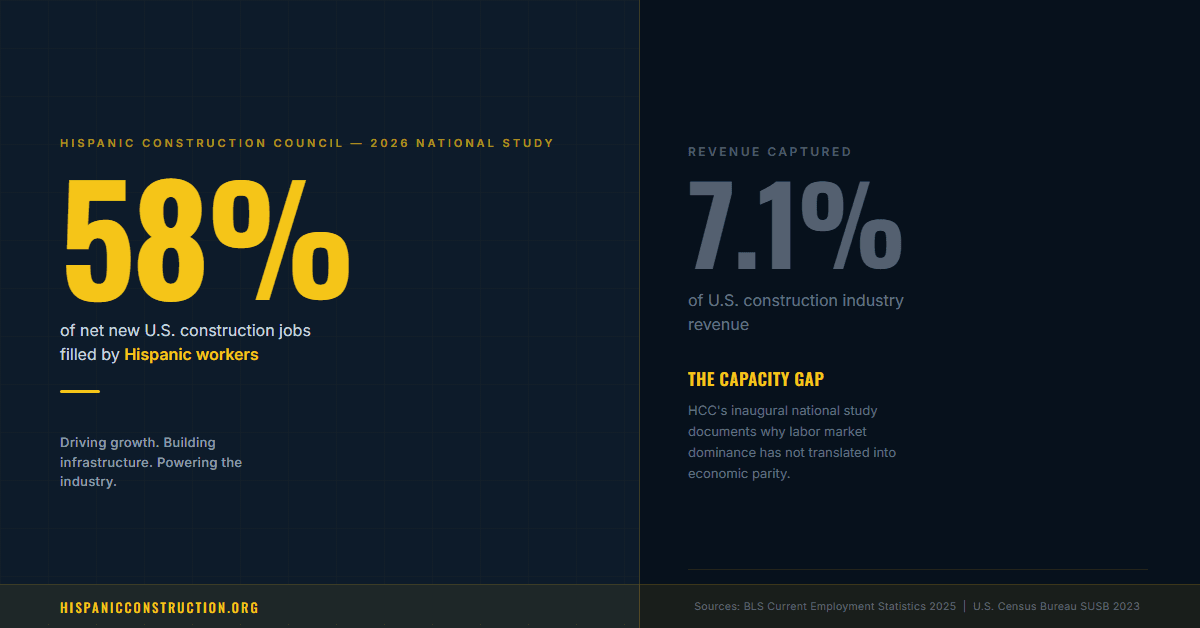

Between 2020 and 2025, Hispanic workers filled 58 percent of all net new construction jobs in the United States. The firms best positioned to convert that labor market dominance into proportional economic power -- Hispanic-owned construction companies -- capture 7.1 percent of total construction industry revenue. The difference between those two numbers is $395 billion a year. This report documents three structural barriers that explain the gap, identifies why those barriers are not about contractor performance, and proposes three specific, implementable policy changes that would close it. No new programs are required. The infrastructure for the solution already exists in partial form.

The Construction Labor Shortage Nobody in Washington Is Naming

The U.S. construction industry reported 375,000 open positions in the first quarter of 2026, according to the Bureau of Labor Statistics. The Associated General Contractors of America projects that number will exceed one million unfilled jobs by 2030 without a significant policy intervention. Average construction wages grew 7.2 percent annually between 2021 and 2026, well above inflation, and the vacancy rate has not closed. Wage increases alone do not fix a structural pipeline problem.

The workforce that has been filling that gap is Hispanic. From 2000 to 2023, the share of U.S. construction workers who identify as Hispanic or Latino doubled, from 16.5 percent to 34.0 percent, per the Bureau of Labor Statistics Current Population Survey. Between 2020 and 2025, Hispanic workers accounted for 58 percent of all net new construction employment. Hispanic-owned construction firms grew at 4.1 percent annually during that same period, five times the industry-wide firm formation rate of 0.8 percent.

Hispanic-owned firms generate $779 billion in annual revenue and employ nearly four million workers, according to HCC's 2025 State of Hispanics in Construction Report. These are not small-market numbers. This is the structural backbone of the construction labor market.

And those firms are 14 percent more productive than the industry average. HCC's internal research found that Hispanic-owned construction firms generate $1.84 in annual revenue per employee compared to an industry average of $1.62. They retain skilled workers at higher rates. They grow faster. They fill vacancies the industry has not been able to fill any other way. The argument that the revenue gap reflects a performance deficit is not supported by a single data point in this study.

An estimated 70,000 qualified Hispanic-owned construction firms cannot access public works contracts because they cannot obtain the bond to bid. Bonding capacity is calculated at roughly ten times a firm's net working capital -- and Hispanic-owned firms entered this industry without access to the generational wealth, banking relationships, and credit histories that provide the baseline for bonding qualification.

Three Barriers Blocking Hispanic Contractors from Revenue Parity

The Capacity Gap identifies three structural barriers that explain the revenue gap. None of them are about the quality of the contractor.

Bonding Access

Surety bonds are required to bid on public works contracts. Bonding capacity is calculated at roughly ten times a firm's net working capital. Hispanic-owned construction firms entered this industry without access to the generational wealth, banking relationships, and credit histories that provide the baseline for bonding qualification. An estimated 70,000 qualified Hispanic-owned construction firms cannot access public works contracts because they cannot obtain the bond to bid. That is a capital access problem, not a competency problem.

Credit and Working Capital

Federal Reserve data consistently shows that Hispanic business owners face higher loan denial rates and receive smaller credit amounts than similarly qualified non-Hispanic applicants. In an industry where contractors routinely finance payroll and materials against contract payments arriving 60 to 90 days later, thin working capital is not a minor inconvenience. It is a ceiling on project size, growth, and bonding capacity.

Prevailing Wage Compliance Complexity

The Department of Labor's 2023 overhaul of Davis-Bacon Act wage calculation rules was the most significant change in 40 years. It raised wage floors in moderate-union markets and created compliance exposure for small subcontractors without HR infrastructure. Large general contractors adjusted. Small Hispanic-owned subcontractors are navigating it without tools, which creates bid deterrence and audit risk on the exact federal projects the Infrastructure Investment and Jobs Act has made newly available.

“The Hispanic construction sector is not a community development story. It is an infrastructure story. The workforce building America's next decade of IIJA-funded projects, AI data centers, and housing stock is disproportionately Hispanic. The firms best positioned to lead that work are Hispanic-owned. The policy infrastructure that would connect their workforce contribution to proportional economic participation already exists in partial form. Finishing it is a policy decision, not a program invention.”

George Carrillo, CEO, Hispanic Construction Council

Key Findings

Hispanic workers filled 58 percent of all net new construction jobs between 2020 and 2025.

From 2000 to 2023, the share of U.S. construction workers who identify as Hispanic or Latino doubled, from 16.5 percent to 34.0 percent. Between 2020 and 2025, Hispanic workers accounted for 58 percent of all net new construction employment nationally. (BLS Current Population Survey, March 2026)

Hispanic-owned construction firms capture only 7.1 percent of total industry revenue.

Hispanic-owned construction firms generate $779 billion in annual revenue and employ nearly four million workers. Yet despite representing 34 percent of the construction labor force and outperforming the industry on productivity, those firms capture 7.1 percent of total construction industry revenue. The gap is $395 billion per year.

Hispanic-owned firms are 14 percent more productive than the industry average.

HCC internal research found that Hispanic-owned construction firms generate $1.84 in annual revenue per employee compared to an industry average of $1.62. They retain skilled workers at higher rates and grew at 4.1 percent annually between 2020 and 2025, five times the industry-wide firm formation rate of 0.8 percent. The revenue gap does not reflect a performance deficit.

An estimated 70,000 qualified Hispanic-owned construction firms cannot access public works contracts.

Surety bonding is required to bid on public works projects. Bonding capacity is calculated at roughly ten times a firm's net working capital. Hispanic-owned construction firms entered this industry without access to the generational wealth, banking relationships, and credit histories that underpin bonding qualification. The result is exclusion from a major segment of the public procurement market.

Federal Reserve data documents a credit access gap for Hispanic business owners.

Hispanic business owners face higher loan denial rates and receive smaller credit amounts than similarly qualified non-Hispanic applicants. In an industry where contractors routinely finance payroll and materials against contract payments arriving 60 to 90 days later, thin working capital constrains project size, growth, and bonding capacity.

The 2023 Davis-Bacon overhaul created compliance exposure that small Hispanic-owned subcontractors are navigating without tools.

The Department of Labor's 2023 overhaul of Davis-Bacon Act wage calculation rules was the most significant change in 40 years. It raised wage floors and created compliance complexity that large general contractors absorbed but that small subcontractors must navigate without HR infrastructure, creating bid deterrence on the exact federal projects the IIJA made newly available.

Three Policy Actions to Close the Hispanic Construction Revenue Gap

None of these recommendations require building a new program from scratch. The infrastructure for each solution already exists in partial form. The gap is in scale, mandate, and measurement.

Raise the SBA Surety Bond Guarantee Program aggregate limit from $9 million to $25 million.

The current ceiling was last adjusted for inflation in 2013. Construction contracts have grown substantially in both scale and complexity since then. A $25 million aggregate limit extends federal bonding access to the mid-market tier where Hispanic-owned firms are best positioned to scale. The SBA guarantee program operates on premiums and has a strong performance history. This is an inflation adjustment with a targeted workforce development benefit.

Require federally funded projects to provide prevailing wage technical assistance to small and minority-owned subcontractors.

The 2023 Davis-Bacon overhaul created compliance complexity that was not accompanied by corresponding support infrastructure. Requiring general contractors on IIJA-funded projects to provide compliance support to their subcontractors, or contracting with nonprofits to do it, would reduce bid deterrence among the subcontractor tier where Hispanic-owned construction firms are most concentrated. Contractor education is a separate problem from tool availability.

Include capital access benchmarks in federal construction contract reporting.

Federal agencies track Disadvantaged Business Enterprise participation on federally assisted contracts. They do not systematically track bonding denial rates, credit utilization, or working capital adequacy among DBE-certified subcontractors. Adding capital access metrics to federal contract reporting creates the data infrastructure for targeted intervention and gives Congress visibility into the structural gap between workforce participation and revenue participation among Hispanic contractors.

What Comes Next for HCC National Research

This is the first of six annual national studies. The data anchoring it comes from the Bureau of Labor Statistics March 2026 Employment Situation, the U.S. Census Bureau Annual Business Survey released November 2025, the HCC 2025 State of Hispanics in Construction Report, and HCC internal research memoranda. Every number in the study carries a source and a date.

The Hispanic construction sector is not a community development story. It is an infrastructure story. The workforce building America's next decade of IIJA-funded projects, AI data centers, and housing stock is disproportionately Hispanic. The firms best positioned to lead that work are Hispanic-owned. The policy infrastructure that would connect their workforce contribution to proportional economic participation already exists in partial form. Finishing it is a policy decision, not a program invention.

Methodology

This report draws on federal labor and business data, Federal Reserve research, and HCC primary and secondary research. Federal sources include the Bureau of Labor Statistics Current Population Survey (March 2026), Bureau of Labor Statistics Job Openings and Labor Turnover Survey (Q1 2026), and U.S. Census Bureau Annual Business Survey (November 2025). Workforce growth and firm formation data draws from BLS CPS longitudinal series 2000-2026. Productivity analysis draws from HCC internal research memoranda cross-referenced against Census ABS employer data. Bonding access analysis draws from SBA Surety Bond Guarantee Program data and industry estimates of qualified but unbonded contractors. Credit access data draws from the Federal Reserve Small Business Credit Survey (2025) and Survey of Consumer Finances (2022). Prevailing wage compliance analysis draws from DOL Davis-Bacon Final Rule (August 2023) and HCC member survey data.

This report was produced by the Hispanic Construction Council Research Department. For data inquiries, contact HCC Research at hispanicconstructioncouncil.org.

Source Citations

- Bureau of Labor Statistics. Current Population Survey. March 2026 Employment Situation. U.S. Department of Labor, 2026.

- Bureau of Labor Statistics. Job Openings and Labor Turnover Survey. First Quarter 2026. U.S. Department of Labor, 2026.

- U.S. Census Bureau. Annual Business Survey. November 2025.

- Hispanic Construction Council. 2025 State of Hispanics in Construction Report. 2025.

- Hispanic Construction Council. The Capacity Gap: How Hispanic Contractors Are Solving America's Construction Labor Crisis and What It Would Take to Finish the Job. April 2026.

- Associated General Contractors of America. 2026 Construction Industry Outlook. 2026.

- Associated Builders and Contractors. 2026 Construction Workforce Demand Report. 2026.

- U.S. Small Business Administration. Surety Bond Guarantee Program. Program data, 2024.

- U.S. Department of Labor. Davis-Bacon Act Final Rule. August 23, 2023.

- U.S. Department of Labor. Infrastructure Investment and Jobs Act Prevailing Wage Implementation. 2022-2025.

- Federal Reserve. Small Business Credit Survey. 2025.

- Federal Reserve. Survey of Consumer Finances. 2022.

HCC Blog | National Study Companion

58 Percent of the Growth, 7.1 Percent of the Revenue

The full blog companion to this study explains the three barriers and three policy actions in accessible form for contractors, policymakers, and media.

Read the Blog Post